EUROPEAN CAR MARKET SEES FIFTH CONSECUTIVE MONTH OF DECLINE IN JANUARY 2019, BUT STILL RECORDS SECOND HIGHEST JANUARY VOLUME OF THE LAST 10 YEARS

- 1.22 million vehicles were registered in January 2019, as volume dropped year on year by 4.6% in the first January decline since 2013

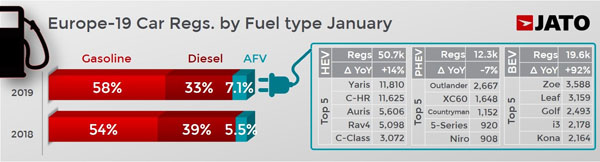

- Diesel car registrations continued to fall, as they counted for just 33% of the total market

- Battery electric vehicles (BEV) led the incline of alternative fuelled vehicles, which finally surpassed the 7% milestone

The European car market registered its fifth consecutive month of decline in January 2019, as registrations fell by 4.6%. However, it was the lowest monthly decline since the introduction of WLTP in September and the second highest January volume of the last 10 years, as 1.22 million cars were registered.

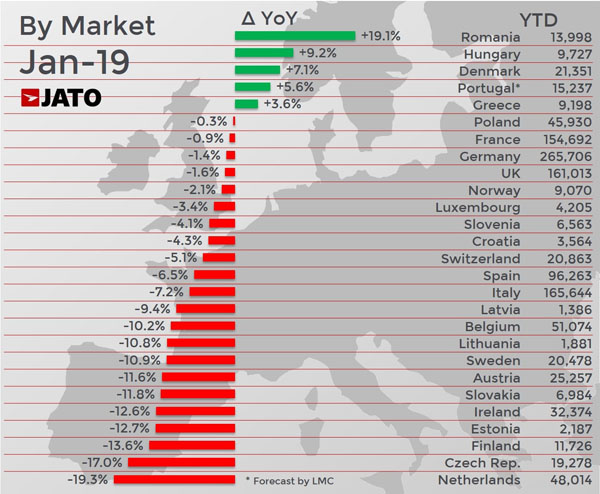

This overall fall in registrations was largely due to only Romania, Hungary, Denmark, Portugal and Greece recording growth. These are all small markets and not big enough in size to offset drops in the big five markets, or double-digit falls in midsize markets like the Netherlands, Belgium and Czech Republic.

The demise of diesel looks set to continue in 2019, as volume fell by 18% in January and counted for just 33% of total registrations. This came as a result of a big decline in Italy, where volume was down by 30%, meaning the country lost its title of being the biggest market for diesels. The Italian market was outsold by Germany – where demand grew by 8% – the only country to post an increase other than Estonia.

Volkswagen, Volvo, Seat and DS were the only brands to post diesel registration increases.

Meanwhile, gasoline cars counted for 58% of total registrations, as volume increased by 2.1%. This marked almost 4 more percentage points than the total recorded in January 2018 and confirms the continuous shift away from diesel and towards gasoline/AFVs.

Alternative fuelled vehicle registrations grew by 22% in January and counted for 7.1% of the total market. Battery electric vehicles (BEV) were responsible for driving this growth, with registrations almost doubling from 10,200 in January 2018 to 19,600 last month. The BEV boom wouldn’t have been possible without the outstanding results of the Renault Zoe (the top-selling BEV in Europe), Nissan Leaf and Hyundai Kona. Meanwhile, Kia recorded 666 registrations of the e-Niro, Jaguar recorded 509 registrations of the I-Pace, and Audi recorded 430 registrations of the E-Tron. “These results confirm that battery electric vehicles are finally taking off thanks to the arrival of SUVs,” comments Felipe Munoz, JATO’s global analyst.

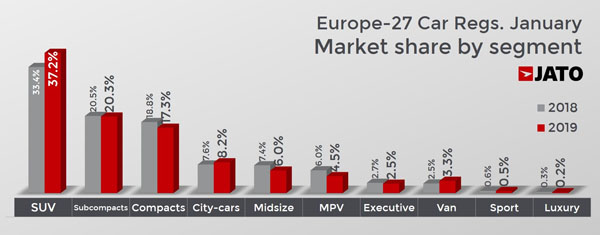

Although SUV registrations continued to grow, there was a significant slowdown to just 6.1%. However, “This can be blamed on the current situation of the European market rather than a lack of consumer interest in the segment,” explains Munoz. The introduction of 14 new models over the course of 2018 also resulted in growth for the segment.

Small SUVs performed well in January with 171,700 recorded registrations. Volume was up 13% as the Volkswagen T-Roc led the subsegment for the first time. Volkswagen also led the compact SUV subsegment, having posted an increase of 4% to 191,000 registrations. Elsewhere, city-cars were the fourth best-selling segment, and also posted an increase thanks to strong results from PSA, Toyota and Renault-Nissan. However, FCA continued to lead, recording almost 30% of the market share.

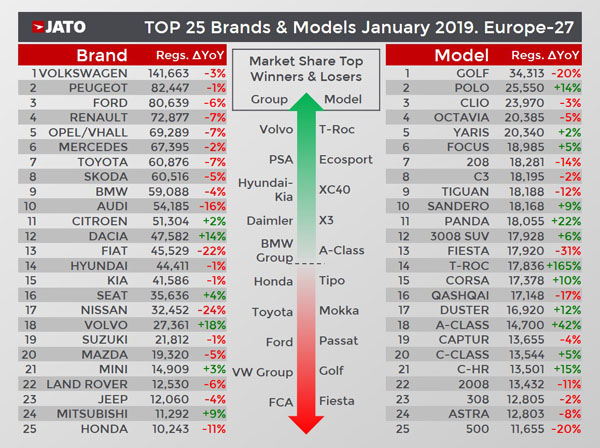

Volkswagen Group continued to lead the market, despite their market share falling from 24.6% in January 2018 to 24.2% last month. The German car maker was negatively affected by big declines at its two main premium brands (Audi and Porsche) as Seat and Lamborghini were the only brands to grow. For the first time, Volkswagen Group sold more SUVs than any other type of car, reflecting the success of its latest launches in the segment, as it was also the overall top-selling SUV maker during the month.

PSA was the second biggest car maker during January, as volume fell by only 2% to 206,100 registrations, equivalent to just 90,000 less than VW Group. Meanwhile, Opel/Vauxhall continued to fall in the rankings, mostly due to growing competition for the Mokka SUV.

FCA saw the highest market share decline, falling from 6.6% in January 2018 to 5.8% last month. It felt the effects of having an aging range, which even resulted in difficulties in its home market of Italy, where it posted the lowest January market share of the last 20 years. With the exceptions of Lancia and Abarth, all other brands posted a decline. Conversely, Volvo was the top market share winner of the month and the only brand to post an increase within the top 10 car makers.

In the Renault-Nissan alliance, the gap between Dacia and Nissan continued to grow, as the former grew by 14%, while the latter fell by 24%, as it also struggled with an aging range, more competition for its super-seller – the Qashqai – and lost the title of being the top SUV seller in Europe.

Ford faced a challenging time in January, as volume dropped by 16% in France, 15% in the UK and 11% in Italy. However, it did achieve a positive result in Germany, where volume was up by 15% to 21,100 registrations, as the country became Ford’s largest market in Europe. The Ford Ecosport excelled in January, with volume up by a huge 166%, while the Fiesta saw a 31% decline.

The Volkswagen Golf was once again the top-selling model; however, it did see a 20% decline in registrations. Contrary to the trend of the last few months, this wasn’t the fault of diesel, but was due to a 26% decline in its gasoline registrations. The Volkswagen Polo was the best performer in the top 10, recording 14% growth in volume, thanks to boosts in Germany, the UK and France. Elsewhere, the Volkswagen Tiguan was the best-selling SUV, despite posting a 12% drop and facing growing competition from its competitor, the Peugeot 3008, which was up by 6%. The Nissan Qashqai, Europe’s top-selling SUV in 2018, fell by 17% overall as its diesel registrations fell by 28%.

Models outside the top 25 that saw big improvements in January included the Nissan Leaf, up by a huge 469%, Ford Ecosport, up by 166%, and BMW X3, up by 60%. There was also progress from the Skoda Karoq (+115%), Renault Zoe (+97%), Hyundai Kona (+71%), Seat Arona (+71%), Mitsubishi Outlander (+64%), Lancia Ypsilon (+55%) and Dacia Logan (+49%).

Among the latest arrivals, the Volvo XC40 was the third best-selling premium compact SUV, and the Audi Q8 was the fourth best-selling premium large SUV, ahead of the GLE Coupe and X6.