- New cars registrations to drop by 1.8% as Brexit settles

- Used car sales to increase by 2.2% in a finance driven market

- Used car supply to be under pressure

- Hybrid and EV sales will accelerate but not fast enough

- Realtime retail driven insight is key to maximising profit

With 2018 consigned to the history books it is important to remember that the industry learnt some interesting lessons during the course of the year. With new car registrations down by 6.8%, almost exactly in line with Cazana’s predictions, and used car sales down by 2.1% it is no surprise that for some the full year results were not as expected and the trading conditions flexed in an unexpected and often difficult way as the months passed.

Key events seem to have crashed into the market one after the other and each one presented a fresh set of problems. From GDPR to WLTP and the often overwhelmingly misinformed debate on new diesel car emissions, there was always an opportunity for both discussion and a fresh approach at improving profit. Such rapid market changes highlighted the importance of quality insight and data provided from observations across the whole market taken from realtime sources and not historical data. Just three years ago many businesses were happy to accept that with a growing new car market and strong used car market, their own historical performance data was adequate on which to base commercial strategy which is by no means acceptable in today’s more complex market.

However, there did appear to be one intrinsically common link between almost every event that took place in the UK automotive sector. Many will have assumed the answer to be Brexit but whilst that played a significant part in many areas of the automotive sector during the course of 2018, the real common difficulty has come in the form of the government. Behind just about every key market changing event has been a controversial government decision or intervention that has been either unjustified or often inexplicable. Indeed, in some cases, just clarification of the decision-making process or of the guidelines issued would make the issues more manageable.

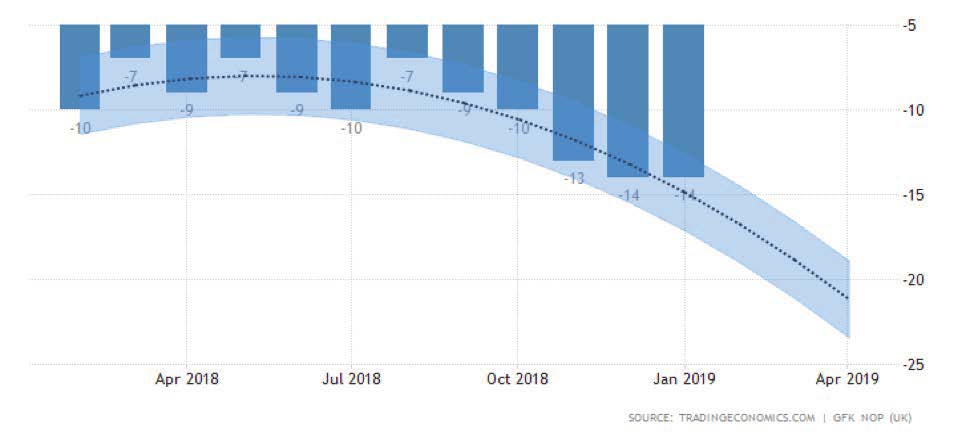

For 2019 the start point needs to look at the greater picture before reviewing key market influencing issues. The chart below shows the 2018 consumer confidence data and forecast for the first trimester of 2019.

Consumer Confidence Forecast

The longer-term view from Trading Economics is that consumer confidence will return to -12 by the end of 2019 and -2 by the end of 2020 so a this means a long and slow recovery period. This is not a positive outlook for the coming months but it is a reality with which the automotive sector and more importantly the country must deal with. Economic growth in the UK has been downgraded too although it is fair to note that there is a similar picture in Europe, albeit less severe, and that is most certainly a reflection of the Brexit position.

Therefore, with low consumer confidence levels and poor UK economic growth seemingly the position during 2019, clarification must be given to a few points. The Brexit position has damaged the automotive sector and the damage is likely to get worse in the coming few months. Whether we leave with a deal or not there will be a period of balance and the country as a whole will need to understand what our new trading arrangements will be with Europe. This will mean that some products may become less readily available and changing tariffs will mean pricing will alter. This may significantly affect the automotive sector for some new cars.

There are signs that key European manufacturers are already trying to stockpile some vehicles in the UK to avoid higher prices. Controversially, the VW Group has been cited as being ready to increase new vehicle pricing (except for Audi) from the day after Brexit, thus passing costs to the consumer. This will be interesting as some of the large German manufacturers have a very large export market in the UK and changing tariffs may mean that altered pricing will see a greater uptake in the UK of home-produced models. This would mean a strange flex in supply and demand that may have long term industry affects particularly on the used market.

Whilst on the subject of new vehicle supply this is one area that is still being affected by the introduction of the new WLTP standard in 2018 and will evolve further during the course of 2019. Whilst many OEM’s tried to deal with this in 2018 there are still issues with some which is manifesting itself by lack of new car supply. For example, Audi sales remain particularly low in relation to direct competitors and the rest of the market with January figures of almost 27% below the same period in 2018 perpetuating the cause for concern given by a full year 2018 registration figure some 18% behind 2017. This is quite a strange position given that sales for the rest of the group had recovered.

Given the volume production constraints, economic concerns coupled with the Brexit debacle and the likely performance of the European new car market this year’s UK new car market is likely to produce registration volumes some 1.8% lower than in 2018 in Cazana’s opinion. SMMT believe the decline in registrations to be slightly higher at 2.3%.

With complications in the new car market it will be the used car market that will be the focus for many of the dealers in 2019. Consumers will seek to spend a little less money and this will be in part facilitated by better used car finance propositions. There are already a number of finance providers seeking to offer more innovative used car funding propositions. The interesting point here is that long- standing finance providers are seemingly moving a little slower and more cautiously than newcomers to the market. This is in part due to their business size but also the newer entrants to the market are using more and better data sources to help with more realistic RV setting resulting in more opportunities to do business driven by realistic deals based on better more accurate GFV’s. The use of retail-based data is key here to help understand what the future value of a car will be and data science is helping by providing fact-based insight untainted by subjectivity.

Greater activity in the used car market combined with a lower volume of stock coming from the wholesale environment as a result of lower registrations in recent years will bring some challenges too. The last two years have seen some real strength in used car pricing driven by retail consumer demand and the transparency that the internet has provided potential buyers has resulted in an acceleration of the change in which wholesale buyers not only search for but also price and source their used vehicles. Working from Retail price back is not a new thing but has become very much more prevalent in the last 12 months and getting the right data to support retail pricing and subsequent wholesale purchasing decisions is more important than ever.

The key is to look for retail driven data sources because that is what the customer does. Ensuring that the data provider researches the whole market and not just a subsection of it is critical. There are many ways to retail a car these days and dealers will continue to be more innovative in bringing the cost of retailing down and improving their profit margin. Having market-wide data that will facilitate profitable trading based on a comprehensive set of market-wide KPI’s will be more fruitful than just seeking the lowest retail price and racing for the bottom of the market. With used car supply constraints already evident this has already proven to be counter-productive.

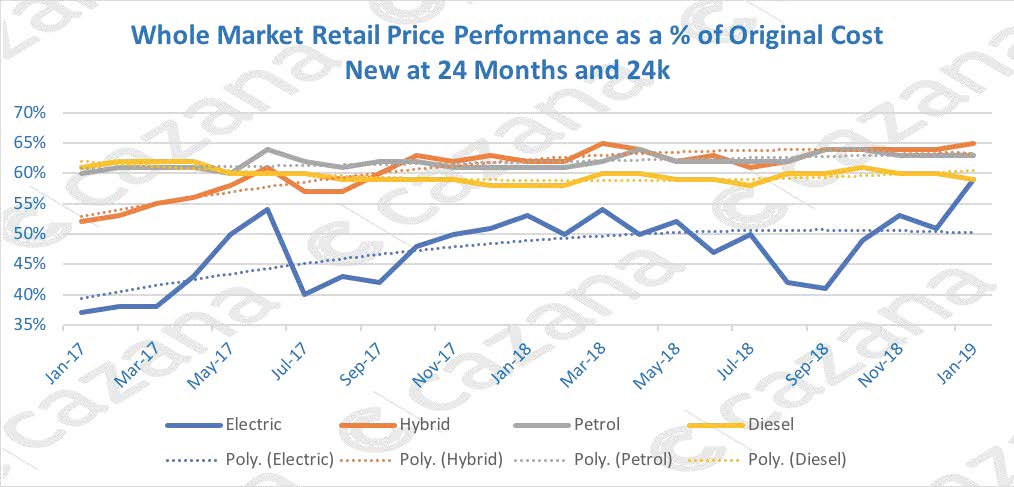

The chart below shows what has happened to retail pricing as a percentage of cost new by fuel type over the course of the last two years: –

Data Powered by CAZANA.COM

This chart is interesting as it clearly shows that retail pricing has been driven by the consumer to reflect an increase in Hybrid vehicle retail pricing from 52% of original cost new in January 2017 to 65% over the course of 2 years. Most of that increase came during 2017 with just a 3-percentage point increase during 2018 suggesting that Hybrids many have found their pricing level. Also, of note is that the pricing and demand for Electric Vehicles are also rapidly increasing. An uplift of 21 percentage points in 2 years is extraordinary although the peaks and troughs in the data highlight the volatility of the pricing which has been largely due to the low data volumes and the type of models hitting the used market. Both petrol and diesel pricing lines show a great level of stability with diesel increasing by 2 percentage points and petrol by 3 percentage points over the period.

In the coming year as volumes of Hybrids returning to the used market increases, the level of retail pricing is likely to tail off slightly. This will be due to the realisation that hybrid ranges do not suit everyone’s needs coupled with the fact that there will be more cars in the market. Petrol prices will probably stabilise and diesel may see a mild drop although this is by no means a given. Whilst wholesale buyers are keen to try and talk diesel wholesale values down the facts are clear. Retail pricing is firm for now. Electric Vehicle pricing is beginning to come of age and this will consolidate during the course of 2019. This will reflect the improvement in not only range but customer understanding as they realise that these cars have a valuable part to play in our future and range anxiety need no longer be a consideration. Infrastructure improvements and clearer messaging from the manufacturer will also help.

The speed with which hybrid technology is improving is impressive although some OEM’s have rushed to get short-range offerings to the new car buyer that will have little appeal when they hit the used market. Clarity from the government on taxation and infrastructure support will greatly help adoption and the new sales figures whilst also consolidating the demand for used variants. There is still a long way to go to meet the somewhat adventurous new vehicle sales targets, but this will be aided during the course of 2019 by the further adoption of low emission zones in cities nationwide. Disappointingly some of the major cities have taken a bit of a step backwards away from somewhat controversial emission charge ideas but this has been partly driven by the greater understanding of the effect these charges would have on local constituents and their voting patterns.

2019 will also see the further development of mobility packages for consumers. The idea that a customer will buy a package charged on a monthly basis giving access to various different types of transport is perhaps a little further away than we might have been led to believe at the beginning of last year. There are a number of companies that have been working on this type of solution but as yet monthly rates have been a little prohibitive and the concept, whilst laudable has yet to gain mainstream adoption by the consumer. Autonomous vehicles also fell afoul of some of this type of over enthusiasm last year and whilst self-driving cars are making progress and will continue to do so during 2019, availability and acceptance is coming far more slowly than anticipated.

Two final points to highlight are firstly, that the diesel discussion will rumble on during 2019. With plenty of used car demand, the new car buyers will eventually realise that Euro 6 engines are not as bad as the national press may have them think. Equally for higher mileage drivers diesel is still a very cost effective and responsible way to travel and until Electric Vehicles have a consistent 350-mile useable range they will not make a dynamic impact on the market.

Secondly, 2019 will have a focus on the sale of multi-driver vehicles. There is growing concern over how the ASA and the courts are handling complaints raised by consumers who believe they were mis- sold their used car. The fact that many consumers seem to believe that a multi-driver vehicle owned by a company is worth less than a privately-owned car is part of the issue. However, condition and history of a car are far more likely to be the price influencer and the way in which a multi-driver car is looked after is arguably more comprehensive and detailed than that of a single driver privately owned vehicle. Unfortunately, the UK “compensation” culture is also a strong driver behind the legal action that may or may not take place.

In summary, the year ahead looks busy to say the least. Once Brexit is either delivered or a plan agreed the economy and consumer confidence will settle. New car registrations will decline by a further 1.8% over the 2018 figure and the focus will shift to the used car market. Innovative used car finance packages will help customers buy the car of their dreams based on accurate transparent dealer pricing and finance companies working with innovative retail driven forecast data will make good business decisions that will not only help the consumer but also their own business by facilitating more business.

Cazana is ideally placed to help every sector of the UK Automotive industry to improve business by providing high-quality realtime retail driven insight that will help improve the return on investment, increase awareness and improve profits. 2019 will be an exciting and innovative year for all.

Written by Rupert Pontin, Director of Valuations at Cazana.com, February 20th.

- Cazana provides global automotive insights, enabling the next generation of vehicle access.

- Founded in 2012, Cazana originally set out to gain a better understanding of the prices of classic cars by using big data. Although it started as a hobby for founder Tom Wood, Cazana has become the largest car search and indexing engine for used cars on sale in the UK. The business now tracks millions of vehicles for sale across eight countries on a daily

- Cazana’s search technology shows every car on-sale, unearths hidden history on every vehicle and tracks a car’s value and history with a timeline of events from manufacturer to present

- Cazana provides a wealth of data to manufacturers, dealers, finance and leasing companies to help them better understand residual value risk and the changing prices of vehicles in the market. Cazana is the first car valuation engine to use real- time retail data and correctly value vehicle condition and specification, which helps its clients price products more effectively and with greater certainty.